Content is King, Again

An upstart upends the media landscape. The company pioneers a new way to distribute shows and movies. Its trailblazing leads its peers and others into a new age of media consumption. But ultimately, the company’s initial distribution advantages fade and the company is forced to compete on content – like everyone else.

No, the passage is not describing the rise and growth of Netflix. Well it is, but it is also describing the rise of HBO. The history of the media and entertainment landscape is filled with these parallels. An upstart makes waves with a new distribution, others soon follow and over time they all compete on the same vector – content.

Rise of HBO

Just like Netflix used the internet to get streaming into the hands of consumers, HBO used satellite broadcasting to create a new category. HBO started as a cable network, customers would have to purchase a subscription through their cable carrier. And in the early days of HBO, the company’s main challenge was getting its content to the 5k+ cable systems that spanned the U.S.

The only way for HBO to reach cable subscribers beyond the New York region would be to cobble together cross-country, point-to-point relay network of microwave transmission towers and existing landlines, which were controlled by the Bell Telephone Company under a broad monopoly. Doing so would cost way more than the network could afford. Much to Time’s dismay, HBO was going nowhere. A year after launching, HBO had roughly ten thousand subscribers.

The company found a hack, however – satellite broadcasting.

About two years into HBO’s faltering life, Levin and his colleagues had an idea. They’d heard that the telecom giant RCA was scheduled to launch a commercial satellite into orbit…Levin convinced the Time Inc. board of directors to invest $7.5 million to rent space on RCA’s “bird” for six years. Levin was adamant. With satellite distribution, HBO could beam shows simultaneously to cable system providers around North America. It could give the network a second chance….

HBO used this technology to get distribution all over the United States. Soon Showtime, TBS, and USA followed in the company’s footsteps. Not only did HBO pioneer this distribution model, but when the broadcast networks convinced the FCC to restrict the type of content that the cable networks could air, HBO sued, won, and prevented the FCC from putting these restrictive rules in place. The lawsuit broadly expanded what the content networks could air and where they could sell their services.

HBO’s innovation and efforts ultimately lowered the barriers to entry into the market. Between 1975 and 2000, the number of cable networks ballooned from less than 20 to >100. To differentiate itself in the increasingly crowded market, HBO started to produce its own content and focused on becoming a leading entertainment company.

And since then HBO has been competing on price and content. And the content output has not been perfect. After the Sopranos ended HBO actually had a bit of a dry spell and allowed their main rival at the time, Showtime to catch up. The company floundered for a few years before finding its next few hits (GoT, Veep, etc.).

HBO’s evolution is remarkably similar to Netflix’s. Both companies were early pioneers of new technology and innovated on the existing content distribution model (Netflix did it twice). Both companies had to evolve to become content producers. Now, HBO almost exclusively competes on that vector. With Reed Hastings stepping down, Netflix is entering a similar phase of the company’s lifecycle – one focused on content.

Netflix is Dead, Long Live Netflix

Under the leadership of Reed Hastings, Netflix rose to the top of the media landscape as a technology company that innovated on the business model and the underlying technology. Back in 2007, when the company first launched streaming, it was challenging and expensive to build a reliable streaming service that could support millions of concurrent views1 (and for some it still is). More importantly, streaming was a worse business than cable. This uncertainty and the investment required to support a streaming service prevented any of the legacy networks from entering the market in a meaningful way.

But those were Netflix’s old advantages – now it’s a content company and has to compete on that basis.

The uncertainty in the market has been resolved – operating a streaming business is worse than running a cable network but cable networks are going to die out. And the technology barrier to launching a streaming network has greatly been reduced.

This is a natural evolution for the company and parallels the technology lifecycle in other industries.

…in markets as diverse as disk drives, accounting software, and diabetes care, the basis of competition – the criteria by which customers choose one product over another changes. When the performance of two or more competing products has improved beyond what the market demands, customers no longer base their choice upon which is the higher performing product. The basis of product choice often evolves from functionality to reliability, then to convenience, and ultimately to price.

So it's fitting that Reed Hastings has handed the reins over to Ted Sarandos and Greg Peters.

Streaming Wars to Content Wars

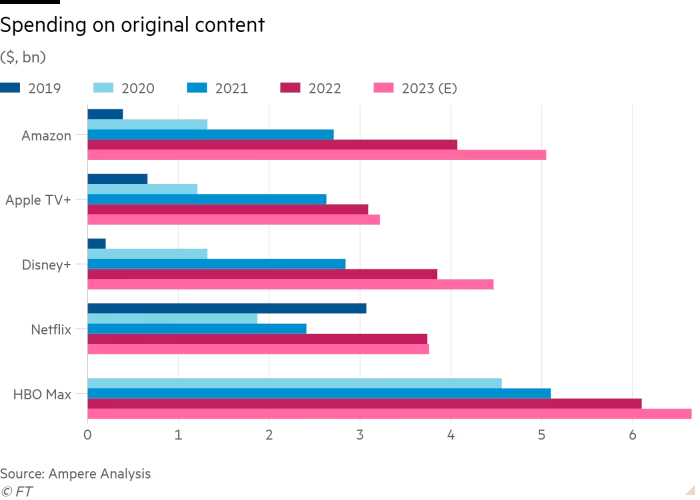

Netflix is by far the leading DTC streamer but spurred by the company’s success and insurgence, others have invested aggressively to scale up their streaming businesses, subscriber base and original content libraries.

Until recently, the price for streaming was relatively uncertain and the legacy media companies had to cannibalize their core business to compete. However, the pandemic and acceleration of cable sub losses over the last 18 months forced the hand of many media executives. While the prize for streaming is still uncertain for many, the prize for not embracing streaming is increasingly certain as well.

Nearly all the top media companies are focused on scaling their streaming businesses. Some, more aggressively than others – and this is increasing the competitive intensity in the streaming market.

More importantly, the investments in the content and decisions to pull content from other platforms are increasing the attractiveness and functionality of each streaming service. A few years ago no one had the technology or the streaming libraries that Netflix had. No one could functionally compete with Netflix on Day 1, which is why many of the streaming services (e.g., Peacock) are launching at low price points.

Here’s Bob Iger on why they had to launch Disney+ at $7/mo.

I also was well aware that we were launching with very little original content “The Mandalorian” was and “High School Musical” were two of them. I think we had five original pieces of content and it would take time. As it turns out, it took more time because of the pandemic to fill that pipeline with enough original content to justify more pricing. As I said yesterday on the earnings call, the price was taken up by $3 from 7.99 to 10.99 just recently, and we had a de minimis, de minimis churn in subs, which says that now that we fuel that pipeline with more original content, and the consumer is also I believe getting more used to using streaming as as a primary source of material that there is pricing leverage and we have pricing leverage.

— Iger’s interview with CNBC (Feb. 2023)

But now that’s changing, the companies have invested in original content, and they have taken back a few key properties.

However, we should expect that Netflix will lose share by any means. The company is a household brand with one of the best streaming products. But the increasing set of viable alternatives for both consumers and content producers is changing the way the company has to compete. The impact will likely be that content costs will continue to balloon and the company’s ability to raise prices in line with investor expectations will become curtailed.

Netflix’s Investor Relations Advantage

This is not the first time that Netflix is faced with a daunting challenge from an incumbent pivoting into its market. Contrary to popular belief, at one point Blockbuster had Netflix on its heels. But Netflix was able to win primarily because of its ability to convince shareholders of its vision and Blockbuster’s inability to do the same.

In 2007, Blockbuster launched a competitive offering to Netflix, Blockbuster Total Access, which allowed Blockbuster customers to order DVDs on the internet and return them in the store. And they eliminated late fees. Soon enough Blockbuster was taking share in the online rental market!

But to compete with Netflix, you had to invest (i.e., burn) money. For Blockbuster that meant eliminating its high margin “late fees” and running promotions/underpricing its digital offering. These drastically cut into the company’s near-term profitability.

For Blockbuster this was a major challenge because they had $1B of debt with covenants that required a minimum level of EBITDA. The solution would have been to fix the capital structure by refinancing the debt and/or raising some equity with a new vision for the company.

Unfortunately, the company ran into two buzzsaws: Carl Icahn and The Great Financial Crisis. Icahn pushed out the management team leading the pivot and replaced the CEO with someone who did not buy into the digital vision.

And it probably did not help that Barry McCarthy was actively going around trying to convince analysts that Blockbuster was doomed.

Peter Kafka: But Gina Keating remembers it a little bit differently. She says Netflix was working really hard, maybe a little too hard to convince outsiders like her, that its strategy made sense and that Blockbuster was gonna fail, and that Wall Street shouldn't give Blockbuster any.

Gina Keating: The funny thing was in the middle of all this stuff, when they started losing subscribers, I went into Barry McCarthy's office in Los Gatos, and he sat there with a whiteboard for about an hour and showed me how there was no way in hell that Blockbuster was ever going to be able to survive this long term because they were losing two bucks for every in-store exchange on total access.

You know, it's kind of funny now when I look back at it, but they were desperate to call a journalist in and spend all this time explaining why Blockbuster should not be able to access the capital markets anymore because it wasn't gonna work.

Peter Kafka: But remember, the reason Blockbuster needed more money from Wall Street was because it was losing money trying to beat Netflix.

And when it came time to refinance the debt, the capital markets were closed. So the company had to file for bankruptcy and Netflix outlasted its most potent competitor.

Netflix had dodged its first bullet.

History never repeats itself, but it does often rhyme

Netflix’s rivals today are similarly positioned – they know they have to transition to streaming but they are saddled with declining profits and a large debt balance. However, there are two big differences this time around.

The cost of not pivoting streaming is known. When Netflix was battling Blockbuster, Icahn and the new CEO were convinced that doubling down on brick-and-mortar was the better decision. They did not see around the corner to streaming and the inevitable death of the DVD rental business.

Management teams at the media companies have convinced shareholders that transitioning to streaming is the prime directive.

Paramount and Comcast (Peacock+) are controlled companies where the management teams and the voting shareholders are one and the same. This is why Iger had to come back – Chapek lost investor confidence during a crucial period for Disney. And activists were pushing the company to make short-term decisions.

Third Point suggested that Disney spin-off ESPN

Trian wanted Disney to do something? Spin-off Hulu?

Fending off any doubt that management had a strong grasp on the wheel was crucial to avoid the company being forced to do anything at the behest of investors (or creditors) that inhibited the transition to streaming.

That’s not to say all is well with the legacy incumbents – some are still stuck in the middle. Warner Bros Discovery has gone back to selling content to Netflix (mostly libraries). AMC Networks is nowhere and James Dolan has effectively told the world that he does not know how to right the ship.

The saving grace for Netflix is that all the companies are burdened with debt and the rising rate environment is curbing investor appetite for losses2. The gross amount that Disney et al could have invested in streaming has been reduced. Everyone has indicated or been forced to say that 2023 will be a peak investment year.

In some ways, the timing has been perfect for Netflix. Interest rates/GFC crushed its original competitor, Blockbuster. Low-interest rates allowed the company to finance its content binging and finally raising interest is curbing its new competitors’ appetite for investing in streaming. But interest rates cut and shareholder fickleness cuts both ways.

From the perspective of shareholders, Netflix is entering the harvest phase of the company’s lifecycle – the company burned FCF significantly to get here and now it’s time to return cash flow to the shareholders. The company’s growth curve looks exactly like what one would expect for a traditional S-curve.

{kind=link}

Netflix is saturated in most of its major markets and top-line growth is expected to slow. Investors now expect growth in FCF/share based on three things:

The average revenue per user (ARPU) will increase >75%

Content spend will moderate

The company will return billions to shareholders in the form of buybacks

All three of those things are effectively contingent on Netflix’s ability to produce content globally at a reasonable cost and provide enough value to consumers that they can consistently raise prices. But in each market, consumers have 3-4 viable alternatives to Netflix all of which today are cheaper than Netflix. And unlike Netflix, its legacy media peers can monetize the content created for streaming and consumer relationships in multiple ways, which means the amount they have to charge for streaming is potentially lower.

More importantly, the legacy media players are comfortable doing a few things that Netflix is not well versed in or wants to be in: sports, advertising, and bundling. And they have a deeper library of hits.

From streaming wars to content wars

This is where we get into a bit of educated speculation. When Iger came back to Disney, people speculated about what he was going to acquire first? But I don’t think his deal-making will be focused on content.

Iger’s most important deal during his second tenure will be to strike an agreement with the other networks and sports leagues to re-bundle the media landscape around sports, news, and Big Four (Disney, NBC, Fox, and CBS). This will establish sports as the center of the OTT universe. The lynchpin for content in the future is going to be sports because in large part it always has been.

A bundle centered on sports would realign the Big Four companies and Warner Bros Discovery3. An underappreciated benefit of all the transactions over the last four years has been that the Big 4 + Warner Bros own a lot of international sports rights.

Disney via Hotstar and Fox Deportes

Comcast via Sky Sports

Paramount via CBS

Warner Bros via Discovery’s various international sports rights

The re-bundling around sports will force Netflix to compete on a regional level. What’s the value of Netflix to a subscriber in Germany when the alternative has Disney+, Sky Sports, World Cup, and the Olympics? In addition to scale, the re-bundling will also solve one of the other pain points that these companies face: churn and seasonality.

The bundle could work because of the growth of a few key aggregators: Amazon, Apple, and Roku. Traditional media companies are already used to having these vendors own the customer relationship and a bundle facilitated by these companies would not be a bridge too far.

Netflix is doing this to a small extent but likely will not lean in because it will lose the customer relationship and risks becoming an undifferentiated “tile”.

The companies that are best positioned to become distributors are Amazon, Apple, Roku, and Hulu. Allying the new bundle with those vendors would also provide a soft landing (if not a tailwind) for the advertising revenues that the networks are losing in lockstep with declining cable subscribers.

Iger laid the groundwork for this recently in his interview with David Faber.

David Faber: But with sports rates going up, Bob as they seem to and with the number of people paying you each month for the linear product, I mean, at what point does it get out of balance and you say, “you know what, we’ve got to take this thing fully over the top.”?

Bob Iger: Well, I think the model ultimately will change. It will become an over the top model. I said yesterday, I don’t know when that will be. We’ve had conversations about it. I actually think as a so-called over the top model, a streaming model, it will be a phenomenal product for the sports fan. So it will give them more flexibility.

David Faber: So one day ESPN will be sort of largely a streaming service?

Bob Iger: One day.

David Faber: But that day is not here.

Bob Iger: No.

David Faber: Do you know when that day comes? Does whoever succeeds you going to know? Like when did you just see it come in like “okay, that’s it. We can’t afford this anymore. We’ve got to try something else.”?

Bob Iger: I should turn the question back to you. If you do the math, you have to – there’s an inevitability to it I believe. But I can’t say when. It will – and we’re not going to do something that’s either precipitous or reckless in any way. We’ll time it right.

The first potential catalyst for the re-bundling is the 2024 NBA rights renewal, which will likely include some version of streaming rights being bid on by multiple players (old and new media).

NBC Sports wants a package that would include playoff games to air on NBC’s broadcast network, two of the people said. Some regular season games could be exclusive to NBCUniversal’s streaming service, Peacock. The NBA could also decide to force media companies to simulcast all games on streaming to increase reach, the people said.

The big hold-up will be getting the sports leagues to go along with the digital rights. But for the sports leagues, a world without a premium bundle to replace the cable bundle would be cataclysmic. Not providing the digital rights for a new bundle will be mutually assured destruction. The leagues in the U.S. are well aware of this reality as they are now dealing with something similar with the collapse of the RSN ecosystem.

In this new re-bundled world, what happens to Netflix? Because of sports, news, ESPN, Disney, and HBO, one would have to expect that the majority of consumers will elect that bundle. Is there enough budget in the consumer’s wallet (or time) to pay for both Netflix and the new age bundle?

Are the company’s content libraries deep enough to justify a position as a standalone vendor?

The answer will ultimately be determined by the company’s ability to produce “must-have” content. And even so, the company might find itself in a position that’s not dissimilar to one AMC Networks finds itself in, on the outside looking in.

Netflix may have to give up on some of its legacy beliefs to compete in the next era of the company’s life.

It may have to buy global sports rights (e.g., Formula 1)

it may have to acquire libraries and production assets to bulk up (e.g., Banijay)

While many have marked this last year as a win for Netflix, I think the company will have to make a lot of tough choices in the next few years, especially with regard to sports. The key question is what does the increasing competitive intensity in the industry do to the company’s ability to increase prices and reduce content spend?

Many of the choices (lower prices, increased content spend, and/or buying sports rights) will likely lead to lower returns than investors are expecting. And will the company whose equity story to date was based on top-line growth have the support from investors to make these choices in a lower growth paradigm?

Getting the technology to compete with Netflix directly was Bob Iger’s primary motivation behind spending ~$4bn to acquire BAMTech. But given the advances in CDN technology and the democratization of services to support streaming, the barrier to building an internet-scale streaming service has meaningfully diminished. If a company wanted to, they could even go the route of spinning up a streaming service exclusively on Amazon Prime Video and use them as a distribution vendor.

See AT&T’s divesture of Time Warner Media

Paramount, which owns CBS, will be the major blocker on this because a significant portion of their EBITDA comes from networks that probably will not be included in the new bundle (nor should they be).

Totally agree with everything here. If these guys ever want to make real money the bundle has to make a comeback - however it is extremely anti-competitive behavior (eg. it’s basically a monopoly).

For the bundle to work, everyone has to play ball though, most people don’t care about sports so having netflix as a cheaper alternative screws up the whole thing I think.

That’s why the Disney bundle is so terrible economically, bundling only works when you are forcing people to pay full price for everything or get nothing, otherwise you just have a bloated package in a competitve market, forcing you to discount (1.99 disney +...)

The interesting question is what happens if it stays competitive. I think the winners will be the smaller players with very targeted, well monetized audiences (‘superfans’). Something like Discovery+ works well, clear demo, low cost per sub because the content is narrow, efficient pricing.. HBO also benefits from having real pricing power and a monopoly on ‘great shows’. WB television is probably worth an NBCU or an Apple TV+. Looks like a very strong combo to compete in general entertainment.

Don’t think Disney+ is viable in its current form, have doubts about PARA, Peacock and the other small ones. Next few years bound to be interesting

The piece didn't touch on the other approach of completely sitting out the content wars a la Sony, and just taking a mercenary view.