Balancing Growth with Margins and the Software Profit Curve

Private equity, activists, and usually passive investors are coming to rationalize software company’s spend and align the cost structure for future prospects. Investors want software/tech companies to strike the balance between growth and profitability. Historically, this has been the requirement and expectation. But we lost our heads and forgot that trees do not grow to the sky. More importantly, investors gave management teams carte blanche to prioritize growth over all else.

Now the market is transitioning to the rationalization phase of the market cycle, and software companies will be required to show meaningful operating leverage. But not all businesses or management teams will be able to.

For some, it’s a lack of experience. Not that many CEOs or CFOs have experienced a bear market.

For some, it’ll be a lack of appetite. After a decade of building a company, some CEOs might be tired, and going through this part of the company’s lifecycle is not that interesting.

For some, it’s hope. Hope that if they invest enough right now, they’ll re-accelerate growth and be the market leader on the otherside. Some might be right, but founders are naturally optimistic (they have to be) and may drive their business into a brick wall.

And it’s not to say that the changes will actually lead to a great financial outcome. The transition from a growth story to a GARP-story (for some, it’ll be a value story) is ugly, and very few companies actually accomplish this. This is typically where private equity comes in and helps reset the story.

Regardless, everyone has one thing in their favor: if managed properly, this transition should not be that challenging from a financial model perspective. The SaaS business model has significant (dare I say, magical) operating leverage embedded in it.

Sources of operating leverage in software businesses

Software businesses have a few sources of leverage:

Sales and Marketing: One of the major drivers of leverage for software businesses and is primarily realized as the company’s net new ARR growth decreases. This impact is largely mechanical since the portion of the company’s cost of acquiring new ARR should effectively decrease (i.e., less sales commission, less required marketing spend to generate leads). The rate at which the company’s net new ARR growth decelerates impacts how quickly the operating margins should increase.

Here’s a simple example that illustrates this point.

The key assumptions are: (a) that the cost of acquiring a $1 net new ARR is $1.50, (b) the cost to support the existing customer base is 20% of ARR, and (c) both costs remain relatively flat1. This is the mental model, but more often than not, software businesses are not managed to follow this framework exactly or unfavorable competitive dynamics limit their ability to do so.

But, even if the business is not managed perfectly, there is still some natural leverage as the company ends up (1) paying less in commissions, (2) renewal fees, and (3) there’s a natural attrition in sales reps. Points (1) and (2) are functions of comp plans2, and (3) ends up being a talent issue (i.e., overall quota shrinks, sales reps don’t meet quota and leave).

However, marketing spending is the biggest opportunity for software companies and the lever that is not flexed enough. Software companies tend to increase their absolute marketing expense irrespective of decelerating growth3. This is in part because of the way companies run budgeting cycles4. But psychologically, reducing overall marketing budget is an admission that the market for their products is saturated, and the company has to transition into the harvest mode of their company’s S-Curve.

So what does the company typically do? Find a new S-Curve, which can take multiple form factors (new regions, market segments, or new products). So the company enters another investment phase to make the “bet,” which sometimes works and most time does not. Unfortunately, some management teams get on this hedonic treadmill and never get off.

There are, of course, exceptions. ServiceNow, Veeva, Hubspot, DataDog, Box, and MongoDB have added multiple S-Curves as public companies. There’s a high correlation between which companies can effectively (and efficiently) create multiple S-Curves and their returns as a public company.

R&D Leverage: This should be a source of leverage for software businesses if the company has a strong market position, but the operating leverage is muted as:

Competition in the core market increases, and the business has to invest to remain competitive / fight-off new entrants.

Companies enter a new investment phase to add S-Curves (“make new bets”).

→ The highest ROI investment cycle for public software businesses in the last decade has been transitioning to the cloud or moving up-market.

The truly special companies in software show incredibly high R&D leverage because they are incredibly smart about extending their existing platform into new products (e.g., ServiceNow). The truly terrible companies are those that maintain high R&D spending but also spend significantly on M&A.

Overhead / G&A Costs: self-explanatory (for most management teams).

What does the trade-off between growth and margin look like?

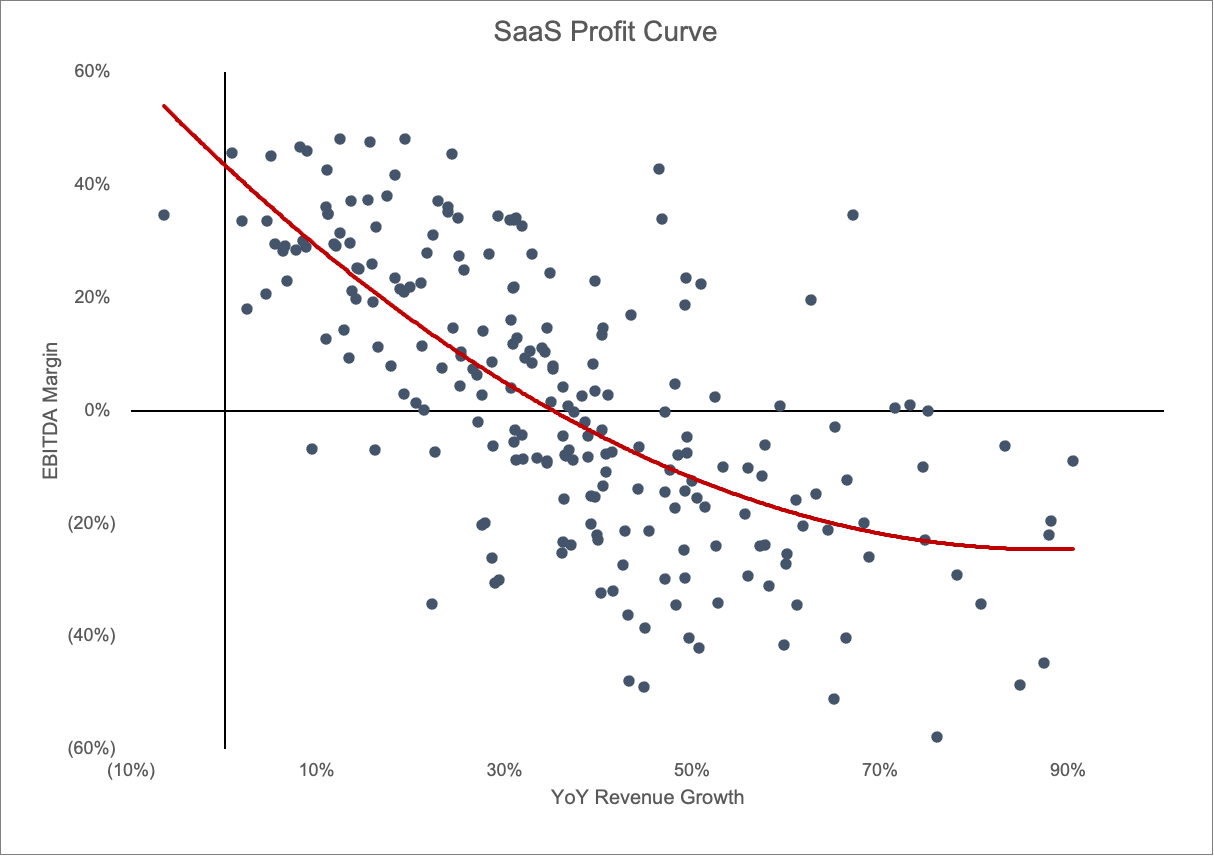

The operating leverage is illustrated by the software profit frontier. The chart below is a scatterplot of the revenue growth of various software businesses and the EBITDA margin over their respective history. To estimate the impact of decelerating revenue on EBITDA margins, we use a polynomial extrapolation to create a “profit curve” for software businesses.

The curve implies that a zero-growth software business should have enough ~40% EBITDA margins with an R^2 of ~48% — and that generally lines up with the SaaS rule of 40. Of course, the data also shows that companies can meaningfully diverge from the profit curve. While easy to put the blame on management, there are, of course, other factors that drive the divergence.

The model businesses that have executed on the profit frontier have been ServiceNow and Veeva, which have diligently balanced growth and profit. Some companies have seen their margins compress as growth decelerates because their end markets became more competitive (e.g., Concur).

The private equity hard “reset”

Companies with strong fundamentals (e.g., low customer churn, favorable competitive environment, and low R&D intensity) but meaningfully divergent from the profit curve will likely have to deal with the prospect of paying the piper (i.e., Orlando Bravo) and a hard private equity reset.

Private equity owners know they can get these businesses to healthy profitability and have the mandate to effect the changes required to balance margins and growth. Again there are many sources of expense reduction that PE owners can implement:

Rationalization of marketing spending to be in line with the current growth profile

Pare back sales rep headcount and investments in

Cut R&D spend in (potentially) low ROI future bets

Raise prices. Boring, but many software companies do not increase prices as much as possible.

In other words, there are a lot of low-hanging levers companies can pull to increase margins as long as the organization can accept growing at the top line (and for managers, headcount) at a lower rate. This is why the (current5) master of the (software) universe6 is circling.

Some special companies/management teams are able to improve this over time with some fairy dust. Companies with product led usage-expansion fall into this category, but increasingly, sales teams are paid to help “drive this usage.”

Most companies pay reps 10-12% on new businesses and less than 3% on renewals. As the business mix shifts to more renewal as % of ARR and less from new business, the commission component of S&M should approach 3%.

Companies do not break out the mix but using headcount growth at public software companies, you can see that marketing headcount generally grows alongside sales.

Unheard of is the software company that runs its budgeting process with a zero-based budgeting philosophy.

It was Tiger Global ~18 months ago, but the Sorceress of Castle Grayskull has smiled upon a new favorite son. She might have been bribed by a private jet to Miami, but those are just rumors.

Fear not. The Master of the (Tech) Universe is still Elon Musk. The Master of the Universe is Jerome Powell.

Solid post and excellent points, as you might imagine, these are active discussions inside of all the SaaS companies (full disclosure, I work for Salesforce). Really appreciate the S-Curve point of view. Found you via Matt Slotnick's thread here: https://twitter.com/matt_slotnick/status/1617591860305793024

Super helpful. Any way to include the names of the companies included? And is each data point a different company or is the same company represented multiple times at different stages?