The Incremental Bid and Shareholder Transitions

Table of Contents:

Understanding the Incremental Bid

Shareholder Transitions

Coupa Case Study

Shareholder Transition En Masse

Programming Note

Understanding the Incremental Bid

One of my early mentors would often say, “Make sure you know who you are going to sell the stock to”. It took me a few years and a few mistakes to fully appreciate what they meant.

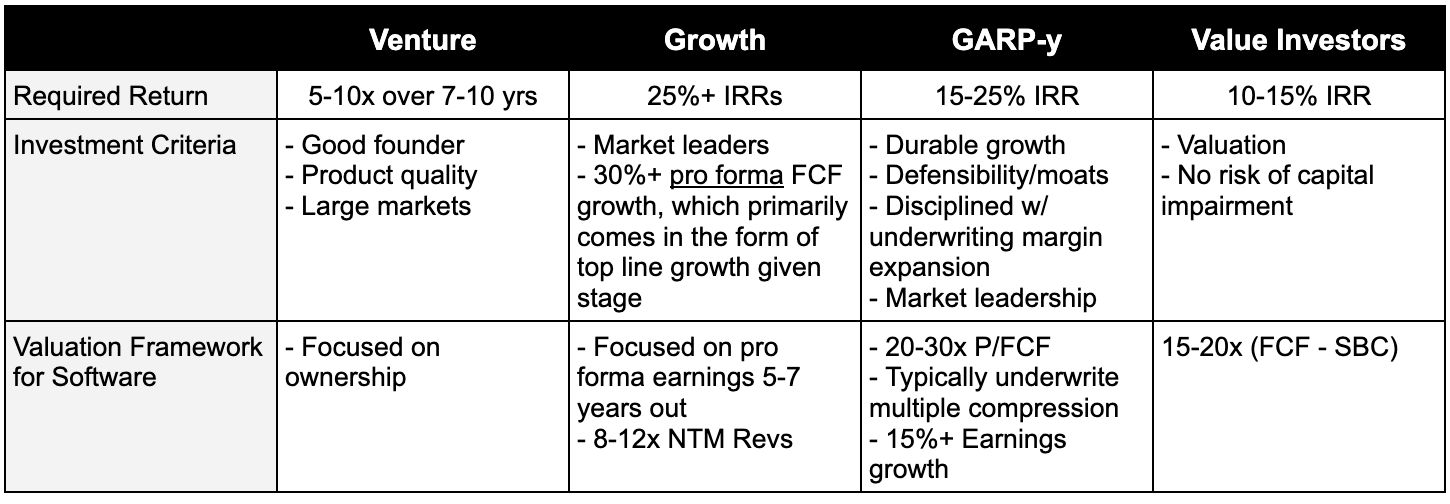

For software/tech companies there are a few classes of investors (venture, growth, GARP, and value). And at a very basic level, the investment characteristics (qualitative and quantitative) for each investor class are different. As a result, the risk premium and price/multiple they are willing to pay are slightly different. Yes, the fundamental characteristics are often similar, but the weightings are different and as a result the risk they’re willing to pay for is different.

Here’s my very rough mental model1 about the investment criteria for different investor classes and the multiple they are willing to pay.

Some of my investing mistakes have been when I’ve failed to properly anticipate what class of investors I would be selling my stock to in the future – and the inverse has been true as well. A few examples that come to mind include

(+) Microsoft’s transition to growth

(+) MongoDB’s re-acceleration with Atlas

(-) Anaplan’s growth deceleration

(-) New Relic’s deceleration & loss of category leadership

(-) Everything about SolarWinds

But often, it's as simple as this meme from a locked account illustrates.

And the focus is not limited to the top line. The qualitative factors2 (product expansion, industry background, competitive dynamics, management team) matter as well.

Is this a category leader?

Given the increasing industry capacity and competition, will Tesla command the same premium multiple in 2-3 years as they do now?

Will Twilio ever be able to transition to effectively selling application software?

The qualitative factors are important because it’s not enough to say that “of course, a company growing at 30% will get a higher revenue multiple than one growing at 15%”. Because if the company growing at 15% is not able to demonstrate operating leverage and a path to 25-30% EBITDA margins in the medium term, the stock price gets hammered. Existing investors rush out the door and there are not many to immediately fill the void. And as a result, the stock will trade at a steep discount to what one would expect for the growth profile.

Managing the transition this transitory period is one of the hardest things for public software companies.

Shareholder Transitions

These shifts in the equity story can lead to shareholder turnover and transition. Shareholder transitions happen when the financial profile and equity story for a company change and the company no longer fit the investment criteria and/or risk profile of the current class of investors. So the current class of shareholders sells their stock and a new class of shareholders takes their place.

These transitions can be smooth or violent but are usually violent. Periods between shareholder transitions can be some of the best times to invest in a business. Here’s an overly reductive overview of a software company’s lifecycle and the shareholder transitions it typically undergoes.

Between each of these transitions, there’s a ravine. Some companies are able to leap over it others fall into the ravine and become stuck, at least for a while. When this happens, the company either becomes:

Orphaned and trudges along

Climbs their way out by either (a) re-accelerating growth in some capacity (new products/markets/segments, M&A) or (b) expanding margins and/or convincing investors they can.

Required to hard reset their shareholder base. This happens both on the public and private side, typically in the form of a buyout of existing shareholders.

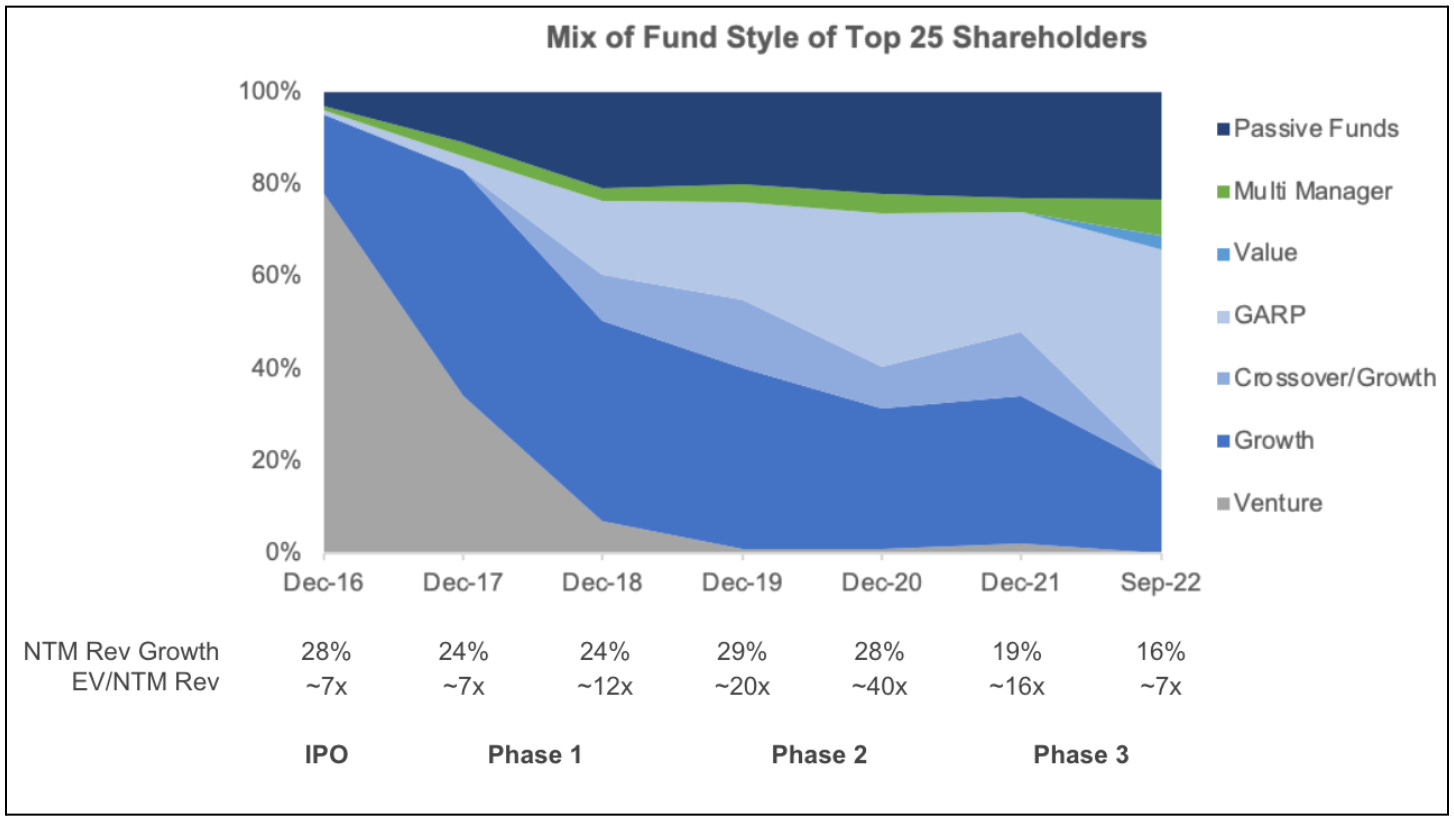

Coupa’s Shareholder Transition

Coupa is a great example of a company that went through the full lifecycle of shareholder transitions. The chart below shows how Coupa’s top shareholder mix shifted in the years after its IPO.

Evolution of Coupa’s Shareholder Base3

Here are the stages of ownership and growth that Coupa went through:

IPO: Coupa went public with venture and growth investors representing 95% of the top shareholders.

Phase 1: Venture investors exited their position and growth/crossover investors took their place.

Phase 2: Investors got bulled up on the Coupa Pay opportunity and growth expectations ticked up from 24% to 28-29%. At this point growth investors and some GARP represented the primary shareholders.

Phase 3: Growth from Coupa Pay did not materialize as quickly as investors expected. Growth expectations fell, growth investors exited the stock and the multiple compressed. GARP-y investors took their place and bought in willing to underwrite mid-to-high teens revenue growth with margin expansion.

At this point, Coupa has two paths in front of it: (1) execute this margin expansion and FCF growth story or (2) go private. Ultimately, Coupa’s business continued to weaken, driven by a weak demand backdrop so management decided to reset the shareholder base. Investors pushed back on the sale.

However, management did not have the confidence (nor appetite) to execute the plan in the public markets. They knew it would be messy and filled with multiple misses, volatility in the share price, and dealing with (sometimes prickly) public markets investors.

In their rebuttal to shareholders, management disclosed that they did not reasonably expect to meet the investor’s timeline for getting back to the Rule of 40. In fact, management expected to meaningfully underperform Street expectations for the next few years.

Shareholder Transition En Masse

There’s a whole set of shareholder transitions occurring en masse right now in the public and private markets for two reasons:

Incremental buyers of risk assets have “left” the market. For the public markets, its been in the form of de-grossing (or reducing exposure to tech). In the private markets, funds have slowed their pace of deployment4.

The capital remaining has reoriented its investment criteria in the face of rising rates. In public markets, investors want companies to strike a healthier balance between growth and spending.

While shareholder transitions are painful and messy for public companies, they’re not terminal (at least in the medium term). For private companies, they can be. The dynamic is important to understand for cash flow-negative private companies because the incremental buyer is the next source of funding.

If a startup does not fit neatly into the investment criteria of the next pool of capital it’ll have to do one of the following:

Get to cash flow positive

Recap the business

Or go out of business

For these private companies, a down-round is not a bad option because the risk of not being investible for the next pool of capital is terminal.

Short Programming Note

Still figuring out the publishing schedule but it will likely be 1-2 posts a week on the following topics:

Software and tech investing (valuation, metrics, etc)

Analysis of companies and certain trends (i.e., AI/ML)

Investing lessons from previous technology companies and trends (e.g., Blackberry, Oracle, Browser Wars)

I don’t plan to do stock ideas for now, but if that’s something people are interested in, may decide to start including it. Let me know your thoughts via email!

Agree this chart lacks a lot of nuances and is very simplistic.

You can probably quantify some of these but those tend to be lagging measures.

The mix is calculated based on # of shares owned by each fund and sub-fund as % of the top 25 shareholders. Fund styles were manually tagged by me based on my knowledge of funds, their other holdings, and fund prospectuses.

This will probably change with the AI hype cycle but only for AI & ML companies, which is why you’ll see/are seeing a whole set of companies trying to “glom” onto the hype train.

Thought this was great. What is the source on your sand chart for Coupa? Are you using CapIQ / FactSet?