Messy Middle and When Religion Isn't Enough

Welcome to Tidal Wave, an investment and research newsletter about software, internet, and media businesses. Please subscribe so I can meet Matt Levine one day.

Given this is an investment-focused post, a quick disclaimer: this is not investment advice, and the author may hold positions in the securities discussed.

Over investment cycles, the attractiveness of industries and asset classes waxes and wanes, largely driven by the flow of capital into said industries and asset classes.

Edward Chancellor describes this dynamic eloquently in Capital Returns:

Typically, capital is attracted into high-return businesses and leaves when returns fall below the cost of capital. This process is not static, but cyclical – there is constant flux. The inflow of capital leads to new investment, which over time increases capacity in the sector and eventually pushes down returns. Conversely, when returns are low, capital exits and capacity is reduced; over time, then, profitability recovers. From the perspective of the wider economy, this cycle resembles Schumpeter’s process of “creative destruction” – as the function of the bust, which follows the boom, is to clear away the misallocation of capital that has occurred during the upswing.

The software sector has ridden this cycle over the last ~10-12 years. For a while, subscription software was the darling. The subscription software business model has all the hallmarks of high-quality businesses: annuity-like revenue streams, low churn, high gross margins, and low incremental costs. All of which should translate to high-profit margins at scale.

For those reasons, investors have historically encouraged all software companies to invest aggressively ahead of those profits. The underlying assumption is as growth slows, the companies' margins should inflect. Ultimately this dynamic attracted capital, valuations increased, and competition for the key inputs (e.g., engineers). As a result, investment returns have suffered and will continue to suffer until companies rationalize their investments and there’s enough “creative destruction.”

Companies that have been able to prove their path to profitability in line with investors’ expectations for the business models will be OK, as will their investors. Those that haven’t are effectively stuck in a messy middle between growth and profit, at least for the next 2-3 years.

Growth over profits (at least for a while)

Mature software businesses, such as Veeva, Autodesk, ServiceNow, and even the much-derided Salesforce, have demonstrated that. The margin expansion/potential is most apparent when the companies begin to climb the "top" of their S-Curve.

Companies earlier in their S-Curves should prioritize growth over profits (within reason). The underlying logic is simply that companies that prioritize growth will get to scale faster and, as a result, generate enterprise value faster.

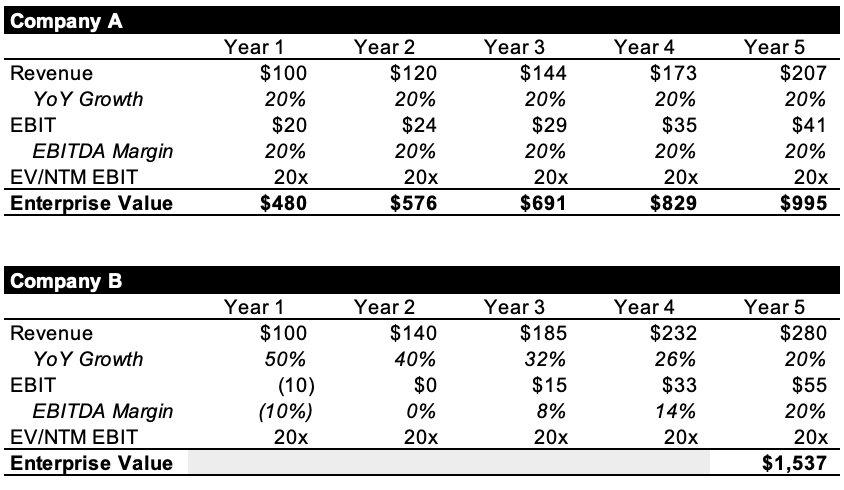

Take this overly simplistic example, Company A and Company B. Both companies start with $100M of revenues in year 1. Company A will grow consistently at 20% and maintain 20% EBIT margins. Company B starts growing 50% y/y in Year 1 but with negative profit margins. Company B’s growth with decay in line with the rule of 80, but its margins will improve in line with the Rule of 40.

By Year 5, Company B is ~50% more valuable than Company A.

This also implies that in Year 1, investors are willing to pay a higher revenue multiple for Company B than Company A, which historically they have. The premium that Company B gets vs. Company A is effectively contingent on what the growth decay investors expect for the company1.

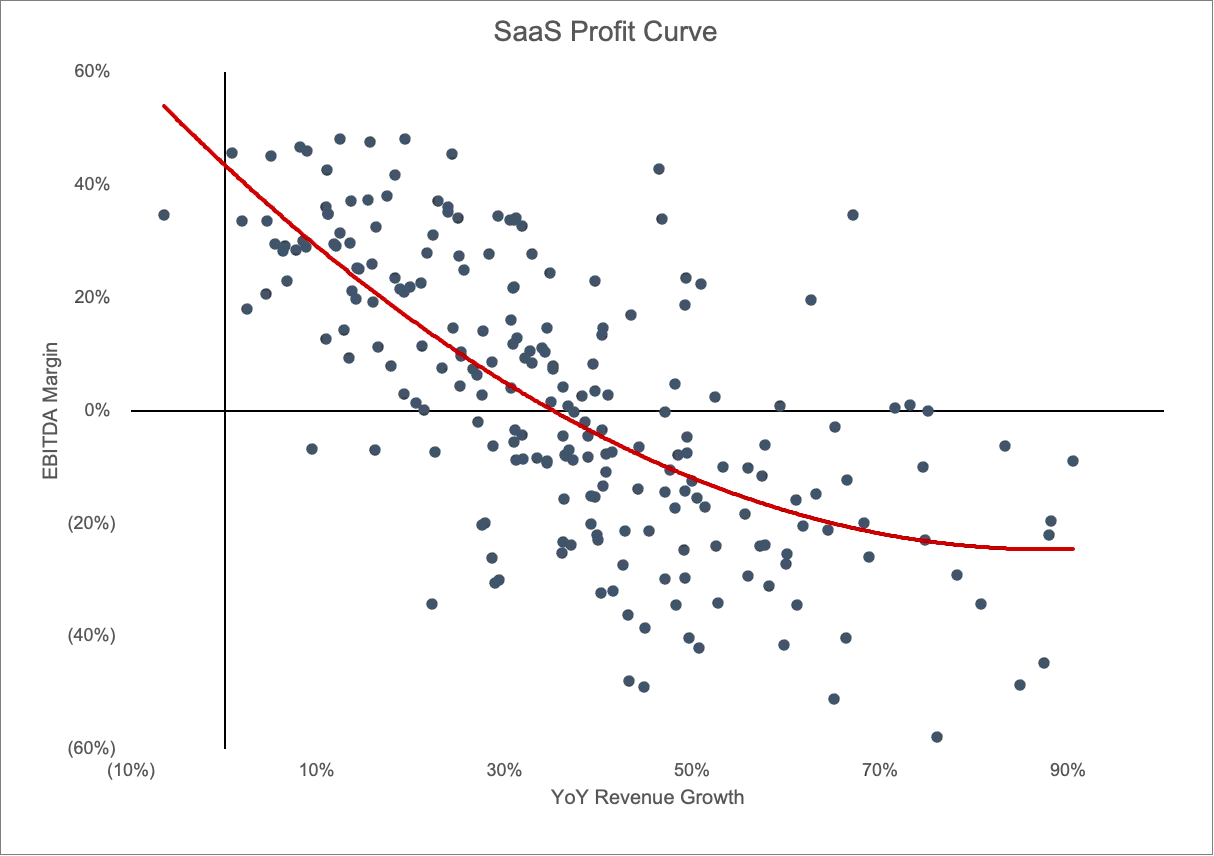

But, investors do not want to be rug pulled in Year 5 by Company B. You don't want to get to Year 5 and find that company is far from being able to get to the 20% margins that you were hoping for. So investors used the Rule of 40, which said that revenue growth plus profit2 should be greater than or equal to 40%. And if you chart the profit margins vs. revenue growth for a broad set of software companies over time, you'll more or less see that profit curve.

Companies that met or exceeded the rule of 40 were rewarded with a premium valuation – and still are. The premium is ~30-50% depending on the company’s growth rate.

Losing the plot

However, over the last ~3 years, the weight (or attention) investors paid for the profit component of a company's growth diminished. And the market writ large focused more on revenue growth. In effect, every SaaS company was given credit for the long-term margin potential that they showed at their IPO and, more importantly, their ability to graciously achieve those margins.

As a result, software, and tech companies more broadly, were empowered to prioritize growth over short-term profits. Since headcount, specifically AEs, is the primary bottleneck for growth for software companies, hiring accelerated. Furthermore, demand pull-forward from COVID made it seem that if you do not hire, you’re leaving growth on the table.

Funding these “growth investments” was cheap because (1) companies could issue equity if they were burning cash, and (2) employees could be recruited with stock comp packages. Employees are willing to take this equity because (1) the headline value is attractive and (2) they can sell the shares after vesting to public market investors, so it was effectively deferred cash payments.

For companies, this was kind of the rational thing to do? If investors are granting you access to cheap capital and your employees are willing to take the capital as payment, then you should, of course, issue as much of it as you can to grow your business.

Incremental opex burden as a leading indicator

The major caveats to this line of thinking are:

Revenue/customers being acquired are accretive.

The investments you’re making are actually driving efficient growth.

Once the period of cheap capital ends, you are able to pare down or unwind the investments.

I’ll quickly touch on the third point first. For both traditional and software companies, the last point is almost 10x harder than what it looks like in a spreadsheet. Unwinding investments are hard for organizations when we’re talking about people, and it takes longer than investors would like it to.

Analyzing (1) is relatively straightforward for software companies, you can look at LTV and CAC paybacks to get a sense. Unless there's an incredibly abnormal activity by the company or the customers, you can probably assume that the ARR acquired is value accretive to the company.

The second point can be monitored with the Rule of 40, but for hypergrowth companies, the absolute growth rate can mask inefficiencies. And Rule of 40 is somewhat of a backward-looking metric. It takes 2-3 years for software companies to recoup the cost of acquiring customers (S&M and implementation), and margin expansion in any given year is heavily influenced by the rate cohorts are maturing. So looking at the incremental Opex spending to acquire new revenue/bookings can be a useful leading metric.

This is effectively a derivative of the rule of 40. If a company (generally) follows the Rule of 40, the incremental Opex should decline as growth slows. So for most software companies, the incremental opex should drop precipitously as growth slows.

And by the time the company reaches the “steady state” of growth, incremental opex should be < 50%, and in effect, incremental profit should be 50%+. But the reality has been more distributed. The table below shows the incremental opex for a sample of application software companies.

Given that all of these businesses have some degree of growth decay, the numbers in each row should be getting smaller. But that’s hardly the case, even if you exclude 2022, which was a period when everyone missed their plans.

You can bucket the companies into a few categories:

Well-managed, defensible, and high-quality software businesses (e.g., Veeva)

Companies that manage to the rule of 40 but are pursuing a durable growth strategy (i.e., very little growth decay), which means the incremental opex does not decline much. Historically both ServiceNow and Salesforce fell into this camp.

Companies that have approached the very top of their S-Curve but are either reaching for growth or facing increasing levels of competition – are the companies in the middle.

Companies that are either not managed well or do not have the levers to get to the Rule of 40 as quickly as investors expect them to (e.g., Coupa and Anaplan).

Companies in the first category are well understood and appreciated.

Companies that fall into the fourth bucket can go one of two ways: (1) they become a zombie company that muddles around as a public company for a while, or (2) they get acquired by a private equity firm. The second is what has happened to Momentive, Coupa, Anaplan, and Zendesk. The low end of the acquisitions has been ~5x NTM Revenues for enterprise companies and ~3x for Momentive. So finding potentially take-out targets given the amount of PE dry powder is still an opportunity.

The Messy Middle

The 2nd and 3rd buckets have the most potential for dispersion over the next two years because most of these companies seem to have “found religion”3 when you look at the incremental opex implied by their guides. That is to say, most of the companies are guiding opex that is in line with what you would expect if the company was following the Rule of 40.

Unfortunately, that’s not enough! Even though most of the companies in the sample above are guiding to incremental opex, which are commensurate with their growth rates, they are far from the Rule of 40. That’s either because the absolute level of opex going into the growth slowdown was too high or the growth deceleration was too much.

To get back to the Rule of 40, companies need to either (1) re-accelerate growth, (2) maintain the level of “austerity” for 2-3 more years, and (3) and/or both.

If the companies in the middle bucket that are trading at 4-6x4 can get to the Rule of 40, there’s a good chance their multiple re-rate 1-2 turns. How long will that take is the key question. Consensus estimates imply that for almost all of them, it’ll take ~3 years. Based on current estimates, that’s a ~1.5-2x return in three years with some dilution. Not a bad outcome, but carries a lot of execution risk and requires underwriting a few turns of multiple expansions.

The other risk for companies that fall into the middle bucket, specifically the mid-cap companies, is that someone opportunistically acquires them before they can execute this strategy in the public markets. The Coupa and HMI back-and-forth is more or less indicative of this.

And as I’ve written about previously, it’s cleaner to make this transition in the private markets if you are the CEO. It’s even more attractive if private equity is promising CEOs that they’ll make money hand over fist.

In summary, SaaS had its own capital cycle of overexpansion, and these companies are facing another 18-24 months of restructuring across the industry. It’s a different backdrop than what SaaS investors have experienced over the last ~10 years, and some of these set-ups (e.g., Smartsheet) might just go to everyone’s too-hard to figure out pile for a while.

If you’re finding this newsletter interesting, share it with a friend, and consider subscribing if you haven’t already.

Always feel free to drop me a line at ardacapital01@gmail.com if there’s anything you’d like to share or have questions about. Again, this is not investment advice, so do your own due diligence.

An average SaaS company follows the rule of 80, but many hypergrowth companies can grow more sustainably.

Some people use FCF, some EBIT, some EBITDA. Not sure why but it does vary between investors. For the purposes of this post, I’ll be using EBIT.

This is an overstated thing, it’s mostly just companies adjusting to the new environment investors are creating.

Hubspot is the odd one out, its growth is not that high, and the company has actually not demonstrated the incremental margins one would expect. So at ~10x, the multiple implies that the company’s growth decay will be better than most, i.e., it can sustain ~20% revenue growth for a long period of time. You can also make the case that Hubspot is still stacking S-Curves with other products, which depress margins.

"I’ll quickly touch on the third point first. For both traditional and software companies, the last point is almost 10x harder than what it looks like in a spreadsheet. Unwinding investments are hard for organizations when we’re talking about people, and it takes longer than investors would like it to. "

Valid, but with the caveat that if the company continues to grow at a decent clip, a hiring freeze (rather than a layoff) can be quite effective.

Thank you for the insightful write-up!

Indeed, it can be argued that both Workday (WDAY) and Okta continue to stack S-curves, which may be causing depressed margins. Workday has been heavily investing in its FINS+ portfolio, likely involving more R&D-intensive efforts compared to traditional SaaS categories but resulting in a stickier product with less susceptibility to tech disruption. Similarly, Okta experienced a hit to its operating expenses with the Auth0 acquisition. Auth0, being a smaller, sub-scale company compared to Okta, negatively impacted Okta's margins. It's evident that Okta mishandled the integration, particularly in sales, adding to inefficiencies.

Regarding the technical analysis, I wonder why operating yield hasn't been considered? Operating yield, defined as Net New ARR / Opex, can provide insights into an organization's efficiency in acquiring net new ARR, assuming net new ARR becomes annuity after the first year. This approach is akin to sales payback but also incorporates R&D and G&A factors.